MTD is now live but with low numbers registered with HMRC, many sole traders and landlords affected are still looking at how to comply, keep the administrative burden to a minimum and will probably be looking for inexpensive – or even free – software to use.

Few sign ups

By early April, about 80% of those who should have registered for MTD hadn’t. The problem is that many don’t see the upside of keeping digital records and reporting figures to HMRC quarterly:

Many people find it hard enough to gather the documents for their annual self-assessment tax return and will not welcome having to comply with strict quarterly reporting requirements:

- The annual self-assessment tax return will be difficult enough for many people to sort out their affairs and they won’t relish meeting tough quarterly reporting deadlines.

- As the MTD compliance threshold is income based, there will be some who will have to comply but will not even have a tax liability. They almost certainly won’t want to pay more agent fees for MTD compliance.

For many, the best option may be to keep the minimum required records with a standard spreadsheet and then use free bridging software to deal with the quarterly reporting requirement. The first quarterly update is due on 7 August so it’s time to get organised.

Software

HMRC has developed a software finder tool that directs taxpayers to appropriate software, including several free options. Many of the options on offer, however, are still in development.

For many sole traders and landlords, software that imports information directly from the taxpayer’s bank account may be the perfect solution, but not if they are putting their business and/or letting income and expenditure through their personal bank account.

Exit Options

The £50,000 MTD threshold from 6 April 2026 is calculated using income for 2024/25. Some people will now have an income below £50,000 and HMRC has explained when it is possible to apply to opt out of MTD.

Unfortunately, opting out is only possible where all sources of qualifying income have ceased; not the case if, for example, self-employment ceases, but there is still property income. Opting out of MTD can be done via HMRC’s webchat, by telephone or by writing to HMRC.

The start point for finding software that works with MTD for income tax can be found here.

Businesses faced some less than funny changes in April including reduced capital allowances, increased fines for late filing of corporation tax returns and the closure of HMRC’s free corporation tax return filing portal.

Capital allowances

Capital expenditure will normally qualify for a 100% first year allowance, but where expenditure does not qualify, a subsequent annual writing-down allowance (WDA) will be given. The main rate of WDA has been reduced from 18% to 14% for periods beginning on or after 1 April 2026 (6 April 2026 for sole traders and partnerships). That means this:

- Most expenditure on cars does not qualify for a 100% deduction, so the WDA reduction effectively results in more tax payable.

- Expenditure on new (not second-hand) zero-emission cars still qualifies for a 100% deduction, although this relief is set to end on 31 March 2027 (5 April 2027 for sole traders and partnerships).

A hybrid rate of WDA will apply for accounting periods spanning 1/6 April 2026.

Penalties

Fines for late submission of corporation tax returns have doubled. The first late filing penalty is now £200, up to £400 if more than three months late.

If the return was also late for the two accounting periods before that, the £200 and £400 penalties are respectively increased to £1,000 and £2,000.

Corporation tax returns

HMRC have closed their free online corporation tax filing service on 31 March 2026, which is no problem for those using an agent. That is:

From now on anyone filing company tax returns with HMRC will be required to use commercial software.

Any changes or amendments to previously filed tax returns will also have to be made using commercial software.

Everything that was once available online, including the HMRC’s tax return filing portal, is now off-limits. Hopefully the records have been downloaded and these should be stored safely.

Companies House was also set to require companies to file accounts using commercial software from 1 April 2027 but this will now be postponed.

The government’s guide to capital allowances can be found here.

Only slightly more than £4 million has been disclosed through HMRC’s cryptoasset disclosure service, possibly a sign of the lack of knowledge and adherence to regulations regarding cryptoassets.

Capital gains tax (CGT) applies to the majority of cryptocurrency gains, and HMRC believes that many investors in cryptoassets have neglected to report their gains when they are sold or given as gifts:

- People may believe that cryptocurrency transactions are tax-free, particularly if they are just exchanging one kind of cryptocurrency asset for another.

- When cryptoassets are added to one of the specialised Visa cards, which can be used anywhere in the world, it is also simple to dispose of them if they are used to pay for goods or services.

For instance, an investor uses some of their Bitcoin to purchase a new cryptocurrency. The investor switches back to Bitcoin as the value of the new cryptocurrency rises. Since both transactions are disposals, gains over the £3,000 exemption are subject to CGT.

Compliance

More than 100,000 letters have been sent by HMRC asking investors to reveal their cryptoasset tax obligations. However, until recently, it was very simple for investors to evade scrutiny by using foreign cryptoasset service providers, who were not obligated to provide HMRC with any information.

On January 1, 2026, new reporting regulations went into effect. These are applicable when a cryptocurrency investor purchases, sells, transfers, or exchanges cryptocurrency assets; however, the reporting requirements have not yet been signed by a number of host countries. Likewise, using a decentralised exchange might circumvent the new reporting rules.

Cryptoassets also pose a problem for inheritance tax (IHT). The assets form part of a deceased’s estate, but access may not be possible when security involves private keys and passwords.

HMRC’s detailed guidance on the new cryptoasset reporting requirements can be found here. Alternatively, contact our accountants in Barnsley.

6 April brings a variety of changes to the tax rules.

The start of the tax year on Monday 6 April (Easter Monday) heralds a variety of changes to tax and pension rules, few of them welcome.

Dividend tax The rate of tax on dividends will increase by two percentage points if you pay tax at basic rate (8.75% to 10.75%) or higher rate (33.75% to 35.75%). The additional rate tax on dividends remains unchanged at 39.35%, as does the dividend allowance at just £500.

Making Tax Digital (MTD) for income tax This starts to operate for the self-employed and landlords who have qualifying income (broadly gross income) from both sources that exceeded £50,000 in 2024/25. MTD will require you to submit quarterly returns of income and expenses to HMRC using approved software.

Inheritance tax (IHT) reforms The new rules for agricultural and business IHT reliefs come into effect. Following changes announced in the Autumn 2025 Budget and two days before Christmas, the 100% relief allowance will be a combined £2,500,000 and will be transferable between surviving spouses and civil partners.

Venture capital trusts (VCTs) The rate of income tax relief for the high risk investments will drop from 30% to 20%. At the same time, the size of companies covered by the scheme will double.

Capital gains tax (CGT) The rate of CGT on gains that qualify for business assets disposal relief will rise from 14% to 18%. Other rates of CGT remain unchanged, as does the annual exemption at £3,000.

National insurance contributions (NICs) If you work or live abroad, then you will not be able to pay voluntary Class 2 NICs (£3.65 a week) to accrue UK State pension for 2026/27 and subsequent years. You may be eligible to pay Class 3 NICs, but the cost is much higher at £18.40 a week.

State pension age (SPA) The phasing in of a new SPA of 67 will begin in April 2026. If you were born between 6 April 1960 and 5 March 1961, then your SPA will increase to between 66 years 1 month and 66 years 11 months. If you were born on or after 6 March 1961, your SPA will be at least 67.

If you would like more information on how any of these changes could affect you, please get in touch with our accountants in Barnsley.

The rate of compensation paid to smaller employers for administering statutory payments will increase from 8.5% to 9% on April 6, 2026, although it will be much less generous than the increase last year.

Employers may appreciate the additional funding, but it won’t cover the cost of the new “day one” rights for all workers or the higher minimum wage rates that will take effect on April 6, 2026.

Recuperation

92% of statutory payments are typically recoverable by employers; however, smaller employers may recover 100% of the cost in addition to the 9% compensation. Thus, starting on April 6, 2026, the overall rate of recovery will be 109%.

For instance, the typical recovery is £920 if statutory maternity pay of £1,000 is paid. A smaller employer, however, will get £1,090 back.

Statutory sick pay is not recoverable, but statutory payments for maternity, paternity, adoption, shared parental, parental bereavement, and neonatal care are.

Employers that are smaller

If an employer’s total class 1 national insurance contribution (NIC) payments for the tax year prior to the employee’s qualifying week were £45,000 or less, they are considered small for statutory payments purposes:

- Class 1A and 1B NICs are not included, but employer and employee contributions are.

- When determining whether the £45,000 threshold is reached, the £10,500 employment allowance is not subtracted. For instance, class 1 NIC payments may be £40,000, but the relevant amount is £50,500 if the full employment allowance is subtracted. It is therefore too high to be eligible.

- The type of leave determines the qualifying week. For instance, the relevant week for statutory adoption pay is the week the adoption agency notifies the employee that they will be matched with a child.

Payroll software uses the employer payment summary to claim relief on a monthly basis.

HMRC’s guide to getting financial help with statutory pay can be found here.

Beginning on April 6, 2026, the State Pension Age (SPA) will be gradually raised from 66 to 67. After SPA is reached, employee class 1 national insurance contributions (NICs) are no longer due, so employers must exercise caution.

Age of pension

SPA will be reached by men and women born between April 6, 1960, and March 5, 1961, at age 66 plus a predetermined number of months. A person born on May 5, 1960, for instance, will reach SPA on June 5, 2026, while someone born one day later will do so on July 6, 2026. For those born on or after March 6, 1961, the pension age will be 67.

Class 1 NICs

Employer contributions are still required even though employee class 1 NICs are no longer due after an employee reaches SPA:

- The first wage or salary payment made to employees on or after SPA is reached is subject to the change. The date of payment, not the earnings period, determines NIC classification.

- For instance, if an employee reaches SPA on or before June 30, 2026, NIC category letter C will be used for the entire June 2026 salary (paid at month’s end).

- To ensure that no more employee class 1 NICs are deducted, employers should verify that the employee’s NI category letter has been set to “C” in payroll software. Depending on the employee’s birthdate, the software might perform this automatically.

The normal procedure is for the employee to show proof of reaching SPA, either with their birth certificate or passport.

The NICs situation on reaching SPA is simpler for self-employed people. After reaching SPA, they simply cease paying class 4 NICs at the beginning of the tax year.

The government’s “check your SPA calculator” can be used to determine SPA can be found here. You can discuss payroll services with our team of accountants in Barnsley.

Employers must be ready for the new “day one” rights, which will take effect on April 6, 2026.

Employers should be aware of the new “day one” rights that employees will have starting on April 6, 2026, even though many of the major changes brought about by the Employment Rights Act 2025 won’t take effect until 2027.

Sick pay required by law (SSP)

Currently, SSP eligibility begins on the fourth day of illness; however, this three-day waiting period will be eliminated:

- All employees will be eligible for SSP after the lower earnings threshold—currently £125 per week—is eliminated.

- Employees who take time off due to illness will be paid 80% of their average weekly wages or the lower of the SSP rate starting on April 6, 2026.

Employers may have to deal with an increase in sick leave abuse cases, which will require careful handling.

Return-to-work interviews and asking employees to check in frequently while on sick leave are two strategies to lessen abuse.

Regular parental leave and paternity leave

Both regular parental leave and paternity leave will become “day one” rights. Currently, paternity leave is only available after 26 weeks of employment; this qualifying requirement will not change with regard to paternity pay.

Currently, unpaid regular parental leave is only accessible following a year of employment.

An employee will no longer be barred from taking paternity leave after taking shared parental leave.

Paternity leave for bereaved partners

This is a “day one” right that was introduced by separate legislation and will become a new statutory entitlement on April 6, 2026. Statutory pay requirements do not exist. Employees who lose a child’s mother within the first year of the child’s life are eligible to take the new leave. Depending on when a bereavement occurs, a maximum of 52 weeks of leave may be taken. If a child is adopted and the primary adopter passes away, the same leave is available.

See government factsheets covering SSP and paternity and parental leave changes or contact our team of accountants in Barnsley for more information.

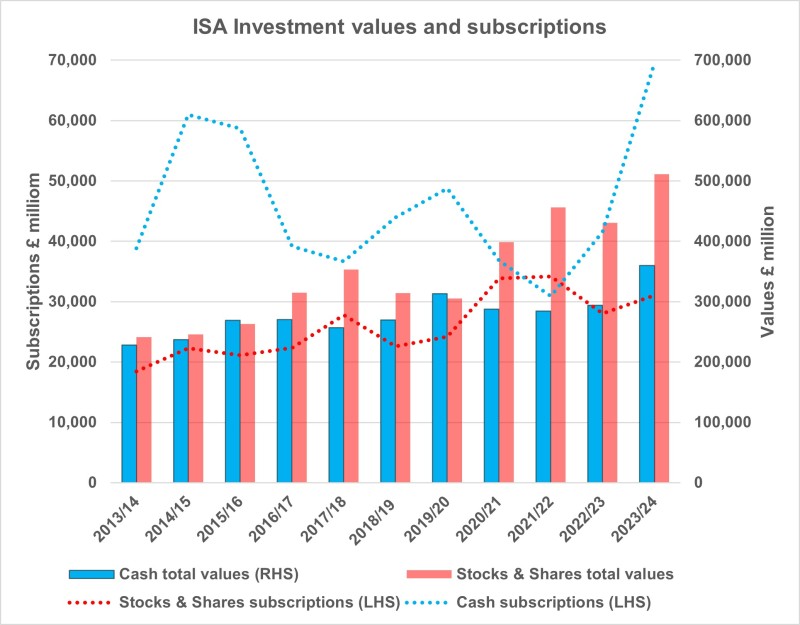

The HMRC figures for 2023–2024 show that subscriptions to cash ISAs have increased by nearly 224% more than stocks and shares ISAs in the decade since 2013–2014.

Source: HMRC.

However, with the 2025 Autumn Budget due at the end of November and ISAs on the Chancellor’s agenda, what does this mean for future savings and investments?

Will the HMRC ISA rules change?

For some time, Chancellor Rachel Reeves has been planning to reform Individual Savings Accounts. It’s widely believed that the current HMRC ISA allowance – the maximum limit of £20,000 per tax year – is going to be reduced for cash ISAs, despite disapproval from the big banks.

The recent statistics from HMRC cast new light on this debate. While stocks and shares ISA subscriptions totalled £31 billion in 2023–2024, cash ISA subscriptions amounted to £69.5 billion, bringing the decade’s total investment in cash ISAs to £360 billion by April 2024.

Assuming this total has now surpassed £400 billion, it would create £16 billion in interest that HMRC isn’t collecting tax on. To the Chancellor, lowering the savings cap on cash ISAs could help to reduce tax loss, as the most recent estimate suggests £9.4 billion was lost in 2024–2025 through untaxed ISAs.

This was up almost 20% from the previous year, after little net inflow for cash ISAs for most of the previous decade when the Bank of England rate was lower and provided worse returns.

It makes sense, then, that the Chancellor would feel justified in changing the rules for cash ISAs – but we will have to wait to see what is announced in the Autumn Budget.

Should you get a cash ISA right now?

Before you rush to set up a cash ISA before the Budget ushers in any changes, you should think carefully about what you want to achieve with your savings deposits.

If you only want to move money to a tax shelter, unless you’re an additional rate taxpayer, the Personal Savings Allowance already covers up to £200 of tax on personal interest.

Or, if you’re aiming to set money aside for long-term growth, there may be better options available.

More details on how ISAs work can be found on the government website, or you can speak to a financial adviser, like one of our Barnsley accountants, to help you explore a range of options.

At gbac, we offer a wide selection of financial services, so we would be happy to discuss tax planning and investment possibilities with you. Simply contact us to talk at a time that suits you.

When used wisely, company loans can be an effective way for directors to access company funds quickly. However, a company loan can also come with serious tax implications.

It’s important for directors to be aware of the ways that taking a company loan can affect their tax liability. Before taking this step, here’s what company directors should know.

Personal tax on director’s loans

Most directors will already know that a company loan could affect their personal tax if there are taxable benefits. If the loan interest is lower than the HMRC rate (3.75%) and the director’s beneficial loans total more than £10,000 during the same tax year, there will be a tax charge.

However, the beneficial loan tax charge isn’t that significant for directors paying the higher tax rate. For example, an interest-free loan of £20,000 for 6 months would only cost £150 in tax.

Company tax on director’s loans

If the individual is the director of a close company and a shareholder, the tax situation will become more complicated. The following rules generally apply to owner-managed companies:

- If a loan is repaid by the deadline for the company to pay Corporation Tax (9 months and 1 day from the end of their accounting period) then there will be no tax charge.

- If the loan isn’t repaid in full by then, there will be a company tax charge in addition to their Corporation Tax bill, applying 75% to the outstanding loan amount.

- The tax charge will be refunded back to the company if the director repays the loan.

This tax charge means that larger loans can become expensive for directors if they can’t repay. The loan will also be a red flag on the company’s balance sheet that may discourage investors or customers.

Get advice on director’s loan tax

If you are a director and borrow money from or pay money into your company, you must keep records of your director’s loan account and include these details on the balance sheet in your annual reports.

More information about director’s loans, and reporting and paying tax on them, is published on the government website. There is also the possibility of outsourcing your accounts management to an agent who can manage your financial records, filing, and taxes for you.

Here at gbac, our accountants in Barnsley can provide a range of services to help company directors with efficient financial management, from corporate finance to tax consultancy and more.

To discuss our accounting services, contact us to book a consultation with our team.